In Florida, insurance is no longer a quiet line item – it is one of the biggest swing factors in whether a rental property makes money. After years of carrier insolvencies, rising reconstruction costs, and relentless hurricane exposure, Tampa Bay owners are paying more for coverage than almost anyone in the country. That makes it more important than ever to carry the right policy rather than the cheapest one, and to understand exactly what it does and does not cover.

This 2026 guide breaks down what landlord insurance in Florida actually covers, the difference between dwelling policy forms (DP-1 vs DP-3), how wind and flood work in a hurricane state, the role of Citizens, and why requiring tenant renters insurance is one of the smartest moves you can make.

This article is general information current as of July 2026 and is not insurance, legal, or financial advice. Coverage terms, exclusions, and the Florida market change frequently. Confirm specifics with a licensed Florida insurance agent before you buy or change a policy.

Why a homeowners policy won’t protect a rental

The most common and dangerous mistake is keeping a standard homeowners (HO-3) policy on a property after a tenant moves in. A homeowners policy assumes the owner lives there. The moment the home becomes tenant-occupied, those assumptions break – and a claim can be denied for misrepresentation. Renting out a home insured as an owner-occupied residence leaves you exposed exactly when you can least afford it.

Landlord insurance – usually written on a dwelling fire policy form – is built for a rented property. It covers the building, adds liability protection, and includes loss of rent that a homeowners policy lacks.

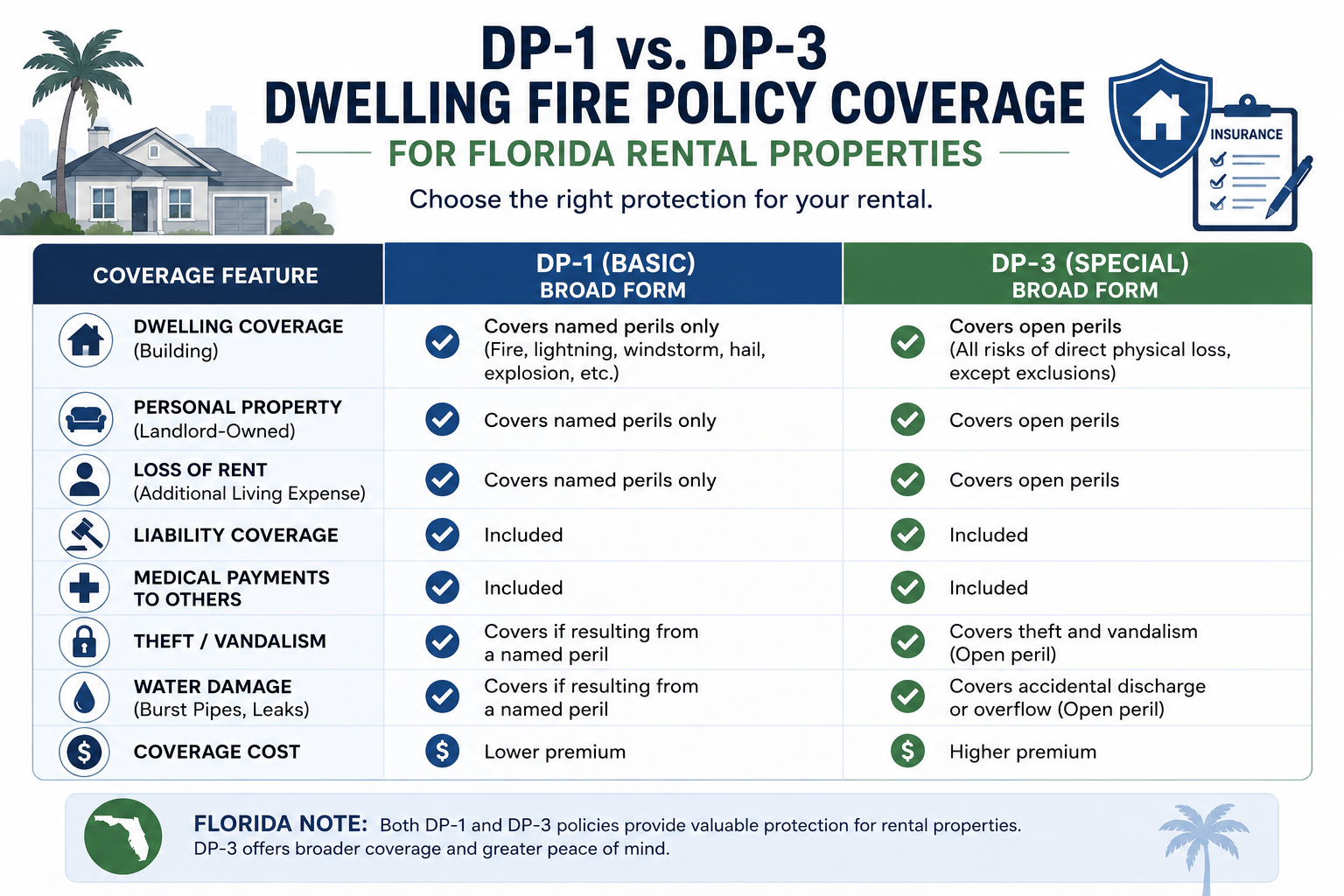

DP-1 vs DP-3: the dwelling policy forms explained

Florida landlord policies are typically written on one of three dwelling fire forms. Two matter most for Tampa Bay owners:

DP-1 is the most basic, named-peril form. It covers only the specific perils listed in the policy and often pays actual cash value (replacement cost minus depreciation). It is the cheapest option and the thinnest protection.

DP-3 is the most comprehensive and most popular choice. It is an open-peril (all-risk) form that covers the structure for any cause of loss not specifically excluded, usually pays replacement cost, and commonly bundles in liability and loss-of-rent coverage. For most single-family Tampa Bay rentals, a DP-3 is the sensible baseline.

If you can afford it, a DP-3 with replacement cost is the standard for a Florida rental. A DP-1 may look cheaper today but can leave a painful gap after a major loss.

What landlord insurance covers – and what it doesn’t

A typical Florida DP-3 landlord policy covers:

- Dwelling / structure – the building, often including attached structures

- Other structures – detached garages, fences, sheds

- Liability – injury claims if a tenant or guest is hurt on the property

- Loss of rent (fair rental value) – lost rental income while a covered event makes the home uninhabitable

What it generally does not cover:

- The tenant’s belongings – that is renters insurance, not your policy

- Flood – almost always excluded; buy a separate flood policy

- Gradual damage, wear and tear, and neglect – including slow leaks and resulting mold

- Sinkhole – often an optional add-on in Florida, not automatic

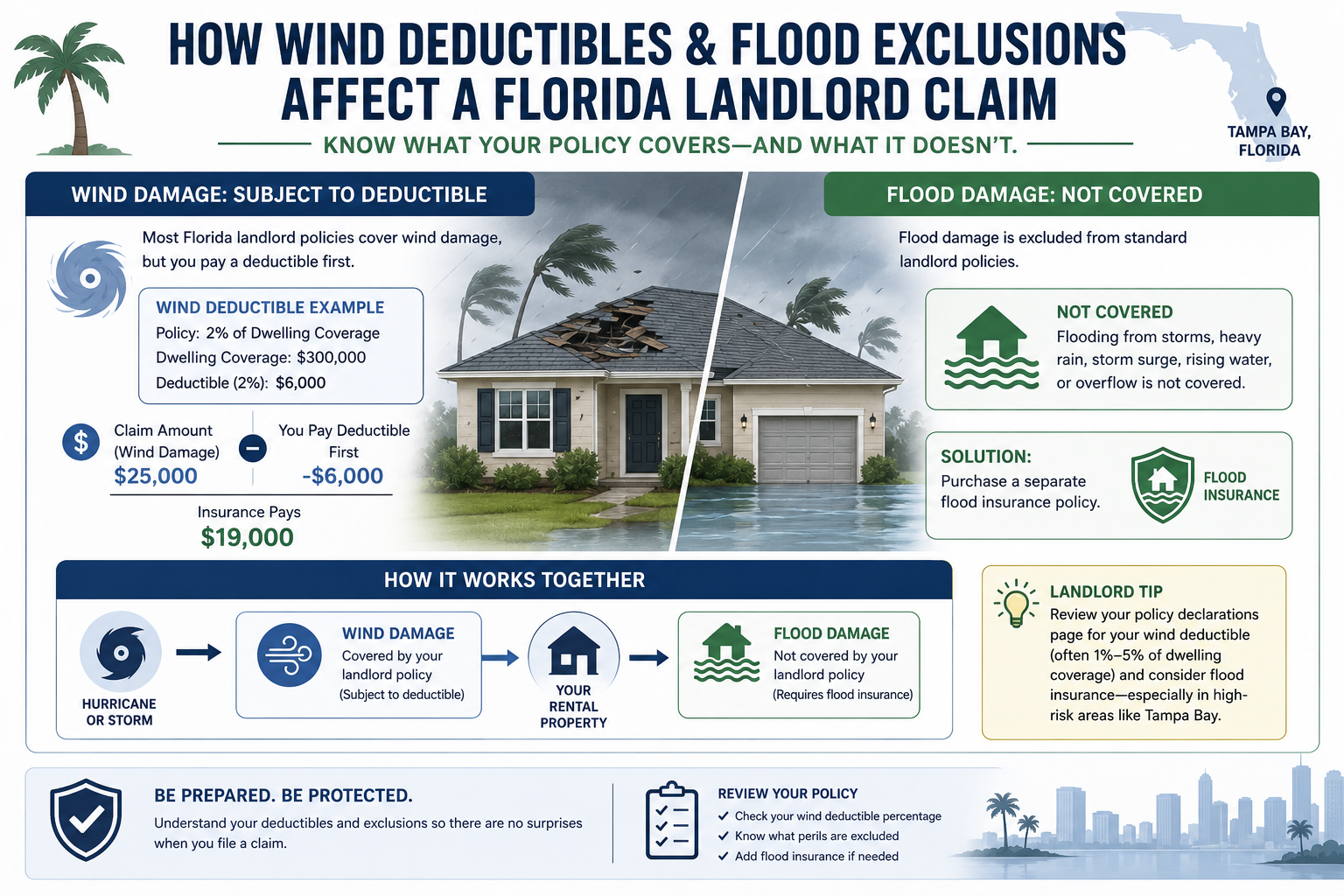

Wind, flood, and the Florida market reality

This is where Florida is different from almost everywhere else.

Wind/hurricane. Damage from named storms is generally covered, but subject to a separate hurricane deductible – often 2% to 10% of your dwelling coverage rather than a flat dollar amount. On a $400,000 dwelling, a 5% deductible is $20,000 out of pocket before coverage kicks in. Know your number before a storm forms.

Flood. Flooding is excluded from standard policies. You need separate flood coverage through the National Flood Insurance Program (NFIP) or a private insurer – and given Tampa Bay’s coastal exposure, it is worth pricing even outside a mapped high-risk zone.

Citizens and the market. Many owners who cannot find affordable private coverage turn to Citizens Property Insurance Corporation, Florida’s insurer of last resort. Citizens has been tightening its rules – including expanding flood-insurance requirements for wind-covered policies – so read the current terms carefully. The Florida Office of Insurance Regulation is the authoritative source for which carriers are writing policies and how the market is changing.

Before you sign, have your agent spell out the hurricane deductible (percentage and dollar amount) and confirm whether flood is included or must be added. These two items drive both your premium and your real-world out-of-pocket risk.

Require renters insurance – it protects everyone

Your landlord policy does not cover your tenant’s furniture, electronics, or personal liability. Requiring tenant renters insurance as a written condition of the lease closes that gap: it protects the tenant’s belongings, provides their own liability coverage, and reduces the odds of a dispute (or a claim against you) after a loss. It is permitted in Florida and is standard practice in professionally managed homes – see our Florida landlord-tenant law overview for how lease conditions like this fit together.

The cost – and the tax angle

Landlord insurance is one of the larger expenses for a Florida rental, with DP-3 premiums on a single-family home commonly running well into four figures a year depending on location, age, roof, and coverage. The silver lining: those premiums are a deductible rental expense. See our rental property tax deductions guide for how insurance and other costs lower your taxable rental income.

If you are just getting started, our guide to buying your first rental property walks through coverage and the other costs to budget for before you close.

A professional manager also helps you stay properly covered – documenting the property’s condition, coordinating inspections that satisfy underwriters, enforcing the renters-insurance requirement, and managing claims if disaster strikes. (Curious how that service is priced? See what property managers charge in Florida

Out Fast Property Management helps owners keep the right coverage in place and handle claims when it counts. Request a free rental analysis and let our team help you protect and optimize your rental.

This guide is general information, current as of July 2026, and not insurance or legal advice. Confirm coverage details with a licensed Florida agent.

Frequently Asked Questions

Do I need landlord insurance in Florida?

Florida does not legally require landlord insurance for most owners, but if you have a mortgage your lender will require dwelling coverage. A standard homeowners policy will not properly cover a tenant-occupied rental, so going without landlord insurance is a serious financial risk in a hurricane-prone state.

What does landlord insurance cover?

A landlord (dwelling) policy typically covers the structure of the building, liability if someone is injured on the property, and loss of rent if a covered event makes the home uninhabitable. It does not cover the tenant’s personal belongings – that is what renters insurance is for.

What is the difference between a DP-1 and a DP-3 policy?

A DP-1 is a basic, named-peril dwelling fire policy that often pays actual cash value. A DP-3 is the most comprehensive form: it is open-peril (covers any cause of loss not specifically excluded), usually pays replacement cost, and commonly includes liability and loss-of-rent coverage – making it the most popular choice for Florida rentals.

Does landlord insurance cover hurricane and flood damage in Florida?

Wind and hurricane damage is generally covered but subject to a separate hurricane deductible (often 2-10% of dwelling coverage). Flood is almost always excluded and must be purchased separately, typically through the NFIP or a private flood policy. Confirm both with your agent.

Can a Florida landlord require tenants to carry renters insurance?

Yes. Florida landlords can require renters insurance as a condition of the lease if it is stated clearly in writing. Your landlord policy does not cover a tenant’s belongings or liability, so requiring renters insurance protects both sides. This article is general information, not insurance or legal advice.