Owning a rental in Tampa Bay comes with a real advantage at tax time. Florida has no state income tax, but the bigger win for most landlords is on the federal side: the tax code is built to reward people who provide housing. Between depreciation, operating expenses, and financing costs, many owners are surprised by how much of their rental income they can legally shelter. The catch is that you have to know which rental property tax deductions exist – and keep the records to back them up.

This is your complete 2026 checklist of write-offs available to Tampa Bay landlords, plus a plain-English look at how it all lands on your tax return.

This article is general information current as of July 2026 and is not tax or legal advice. Tax rules change and depend on your specific situation. Always confirm with a qualified CPA or tax professional before filing.

How rental deductions work: meet Schedule E

Most individual landlords report rental income and expenses on Schedule E of Form 1040. You list the gross rent you collected, then subtract your deductible expenses and depreciation for each property. What remains is your taxable rental income – and the goal of smart record-keeping is to make sure every legitimate expense actually shows up on that form. The IRS lays out the rules in IRS Publication 527, the residential rental property guide every owner should bookmark.

The big four: mortgage interest, taxes, insurance, depreciation

Four deductions do most of the heavy lifting for a typical Tampa Bay rental.

Mortgage interest. The interest portion of your mortgage payment on a rental is deductible, and on a financed property it is often the single largest write-off.

Property taxes. Florida property taxes on the rental are deductible as a rental expense on Schedule E.

Insurance. Premiums for your landlord (dwelling) policy are deductible – which matters a lot in Florida’s expensive market. See our guide to landlord insurance in Florida for what coverage you actually need.

Depreciation. This is the deduction owners most often leave on the table.

Depreciation: the deduction you don’t write a check for

Depreciation lets you deduct the cost of the building (not the land) over 27.5 years for residential rental property using the IRS’s MACRS schedule. It is a non-cash deduction – you are not paying anything in that year – yet it directly lowers your taxable rental income. On a $300,000 building value, that is roughly $10,900 a year in deductions.

Investors who want to accelerate those deductions sometimes use cost segregation for real estate investors, which breaks a property into shorter-lived components (5-, 7-, and 15-year property) that can be written off faster.

Your settlement statement and an appraisal help you split the purchase price between land and building – the basis for your depreciation. Keep them with your permanent records.

Repairs vs. improvements: the distinction that trips landlords up

This is where audits happen. A repair keeps the property in working order (fixing a leaky faucet, patching drywall, repainting) and is generally fully deductible the year you pay it. An improvement adds value, extends the property’s life, or adapts it to a new use (a new roof, an addition, a full kitchen remodel) and must be capitalized and depreciated over time.

The fastest way to lose a deduction is to call an improvement a repair. When in doubt, ask your CPA.

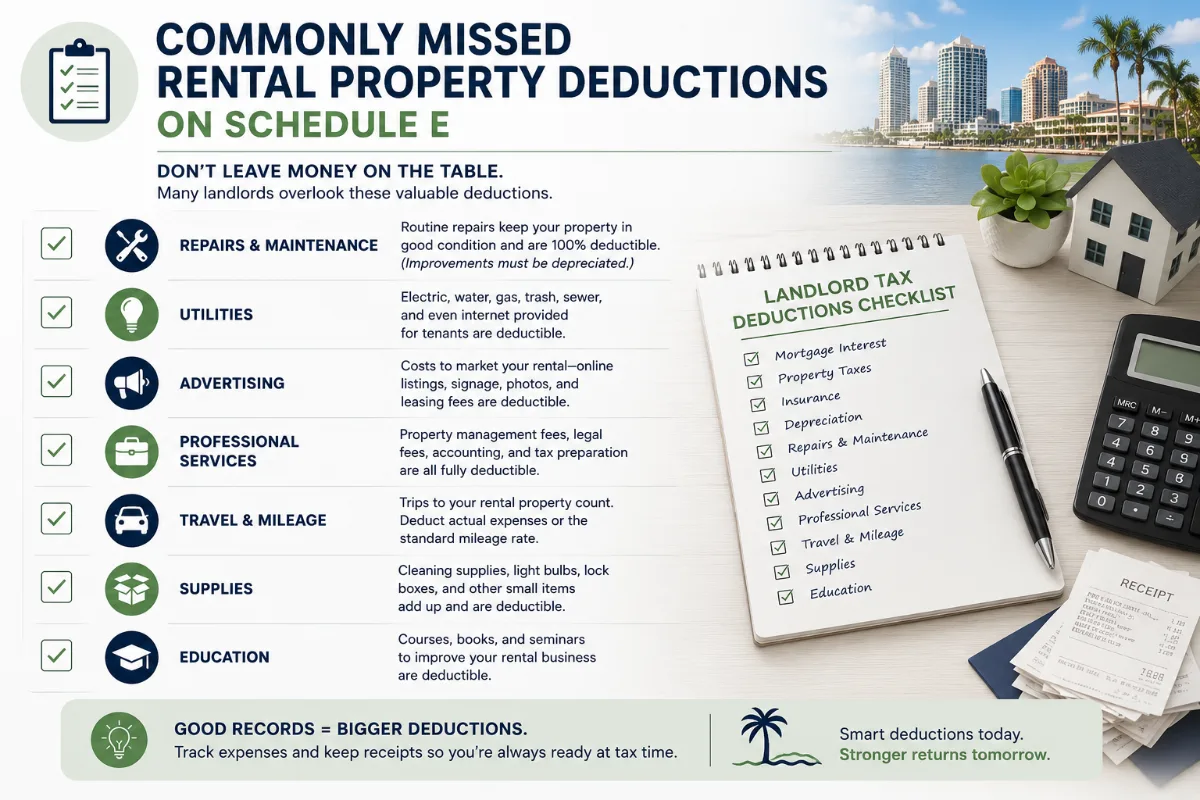

Operating expenses landlords forget

Beyond the big four, these everyday costs are deductible on Schedule E:

- Property management and leasing fees – fully deductible. (Curious what those cost? See what property managers charge in Florida.)

- Advertising and listing costs to fill a vacancy

- Professional fees – legal, accounting, and tax prep tied to the rental

- HOA and condo association dues

- Utilities you pay on the tenant’s behalf

- Travel to and from the property for management or maintenance

- Supplies, tools, and turnover cleaning

Recordkeeping: deductions you can’t prove don’t count

The IRS expects documentary evidence – receipts, canceled checks, invoices, and bank statements – for the expenses you claim. The owners who keep the most in deductions are simply the ones who keep the best records. New to this? Our guide to buying your first rental property covers the records to start collecting from day one. A property manager helps here: a good one delivers a clean year-end statement that maps your income and expenses straight onto Schedule E, which is one more reason management fees often pay for themselves.

Out Fast Property Management gives Tampa Bay owners organized monthly and year-end statements built for tax time. Request a free rental analysis to see how professional management protects both your property and your paperwork.

This guide is general information, current as of July 2026, and not a substitute for advice from your own CPA or tax professional.

Frequently Asked Questions

Is a property management fee tax deductible?

Yes. Property management fees are an ordinary and necessary rental expense and are generally fully deductible in the year you pay them, reported on Schedule E (IRS Publication 527). See our guide to what property managers charge in Florida for how those fees are structured.

What rental property expenses can Tampa Bay landlords deduct?

Common deductions include mortgage interest, property taxes, insurance, repairs, management and leasing fees, depreciation, advertising, professional fees, utilities you pay, travel for the rental, and HOA dues – all reported on Schedule E.

What is the difference between a repair and an improvement for taxes?

A repair keeps the property in working condition and is generally deducted in full the year you pay it. An improvement adds value or extends the property’s life and must be capitalized and depreciated over time (27.5 years for residential rentals).

How does rental property depreciation work in Florida?

The IRS lets you depreciate the building (not the land) over 27.5 years for residential rental property using MACRS. It is a non-cash deduction that lowers your taxable rental income each year you own and rent the property.

Do I need a CPA to file rental property taxes?

It is not required, but rental taxes get complex fast – depreciation, repairs vs. improvements, and passive-activity rules all have traps. A CPA or tax professional often pays for themselves through deductions you might otherwise miss. This article is general information, not tax advice.